By

The USS Abraham Lincoln conducting blockade operations. Source: U.S. Navy/Getty

Get the Latest US Focused Energy News Delivered to You! It’s FREE:

- The Strait of Hormuz remains blockaded — latest peace efforts have fizzled.

- European assets are sustaining far more damage than the US from the stalemate.

- The US K-shaped economy is holding up well, for now.

The US Is Winning the Blockade

The Strait of Hormuz has now been double-blockaded — by both the US and Iran — for three weeks. There’s a “ceasefire,” in terms of no longer bombing terrestrial targets, but both sides continue to use force and threats of violence against each other while ratcheting up damage.

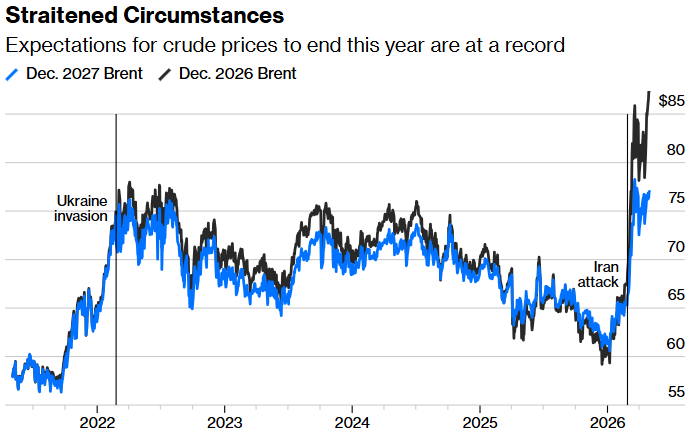

Who exactly is winning? The most obvious case is that the standoff, by throttling supplies of oil and other vital commodities through the Strait, is building up the economic pain for the US and its allies. It takes time for oil to cross oceans and reach its destination, and for well-established inventories to deplete, but markets say the effects will be tough and lasting. Brent crude for the end of this year is at a new high, while 2027 prices are also elevated:

Source: Bloomberg

It’s obviously not an acceptable long-term position for the US, which is now launching a new plan to help ships through Iran’s blockade. But financial markets are behaving as though the war is over. That is a critical advantage for the US. Robin Brooks of the Brookings Institution argues strongly here that the blockade is working. He breaks down the strategy into three effects on Iran: starving it of exports, forcing it to run out of storage capacity, and capital flight. The first two take time to hurt, but he suggests capital is already fleeing.

Meanwhile, markets can create their own reality and stymie Iran’s greatest weapon — economic damage from blockading the Strait. Stocks are at a record and volatility is low. That’s partly down to the luck that the AI trade has resurged in the last few weeks. It’s also aided by the belief that Iran’s position is so weak that it will have to thrash out a compromise over Hormuz without forcing the US to commit ground troops. Brooks argues:

If the blockade is credible (which I think it is), in the market’s mind it may shorten the duration over which the SoH stays closed (since it increases pressure on Iran to do a deal). So the fact that markets haven’t freaked out is a combination of that and the fact that US data and earnings have been generally favorable.

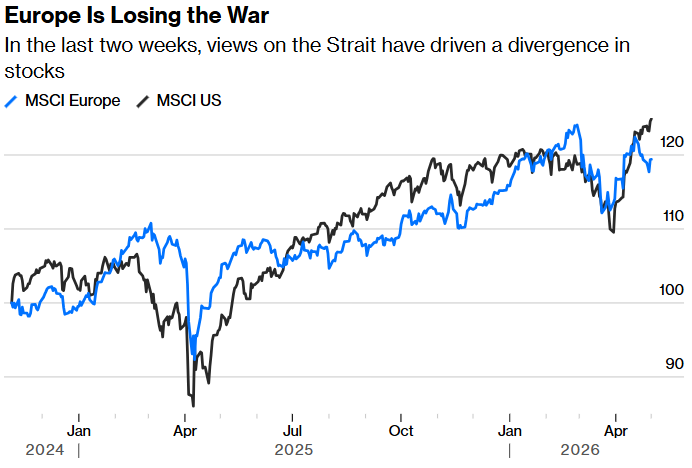

If the US is winning from the impasse, though, Europe is losing. The double-blockade has seen European stocks sell off as the US has rebounded, testament to the extra jeopardy caused by the continent’s reliance on the Strait:

Note: Data is normalized with factor 100 as of Nov. 5, 2024.

Source: Bloomberg

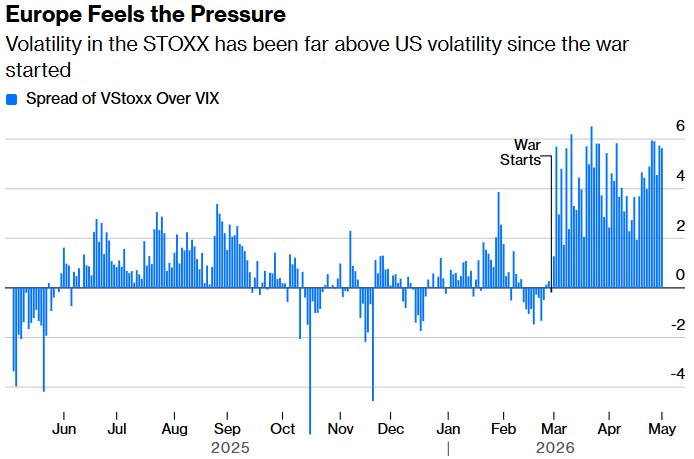

Since the outbreak of the Iran war, investors have assumed that European stocks have more at stake, with volatility of the Stoxx indexes much higher than the S&P 500:

Source: Bloomberg

In the last few days, the continent’s problems have multiplied as the US announced both fresh tariffs on European cars and a drawdown of troops from Germany. This looks like kicking a man when he’s down. It’s easier to score a victory over an ally who has assumed for generations that you’re a friend, a cynic might argue, than to beat an enemy in constant readiness to hit back at you.

But the punishment of Europe might yet prove an Achilles heel for the US. A weaker and poorer Europe would buy fewer US exports and create even more geopolitical difficulties. For the time being, though, the calculation is that this is collateral damage the US can live with, and the market agrees.

Constant Pain

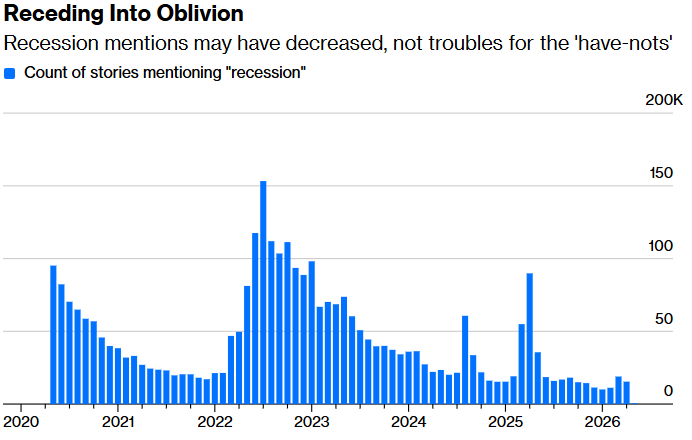

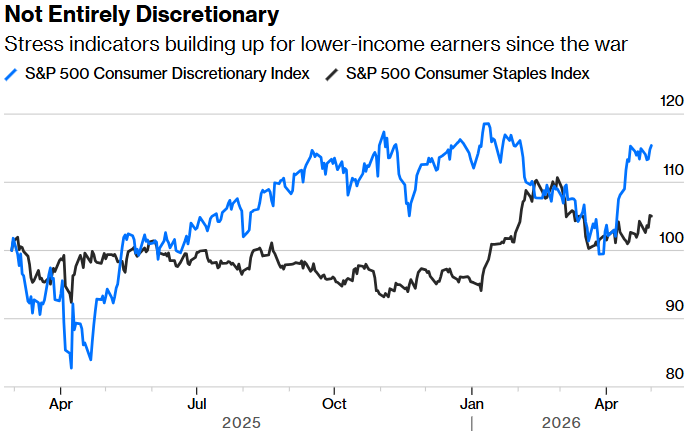

After the pandemic, as the Federal Reserve wrestled to rein in runaway inflation, the US economy flirted with recession. But somehow, it kept soaring, largely propped up by the unprecedented spending on artificial intelligence by mega caps. But while its continuing strength is an advantage for the US in its war, the recession for lower-income earners grows ever more obvious. That fueled the affordability crisis that propelled President Donald Trump back to White House. Mentions of “recession” have collapsed since their 2022 peak, but little suggests that the “have-nots” are basking in the glory of the near-perfect wartime markets:

Source: Bloomberg News Trends

Trump’s tariff brinkmanship and then his military campaign in Iran have threatened to reignite inflation, with gas prices at the pump now exceeding $4 a gallon. A recent rally in consumer staples shows the growing strain as consumer confidence sinks to fresh lows.

How to make sense of this? BCA Research’s chief strategist, Felix Vezina-Poirier, notes that while markets are driven by the economy, they also drive economic life through financial conditions, wealth effects, and input prices. That wealth effect is especially important in a K-shaped economy: consumption for the upper part of the K depends on capital income and wealth effects, while the lower part depends on wages.

Consumer discretionary stocks have lagged, largely thanks to their lack of tech firepower, but they’re staging a respectable rally. It looks like the “haves” remain in the game and are spending money:

Note: Data is normalized with factor 100 as of Feb. 27, 2025.

Source: Bloomberg

The New York Fed’s Economic Heterogeneity Indicators show retail spending driven by high-income households earning more than $125,000 per year. To quote the bank’s researchers, “reliance on a single segment of the economy has important implications for spending growth and its fragility, as well as for economic vulnerability and policy.”

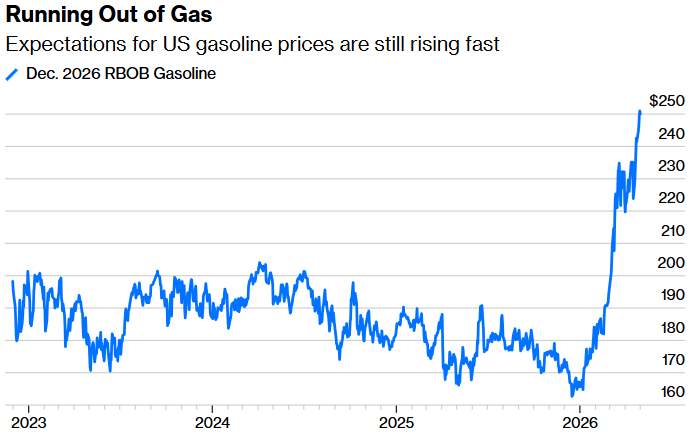

How long can lower-income households hold out? The temporary boost to incomes from tax refunds is fading now that tax day has passed. Sam Tombs of Pantheon Macro sees this leaving households increasingly exposed to surging gas prices.

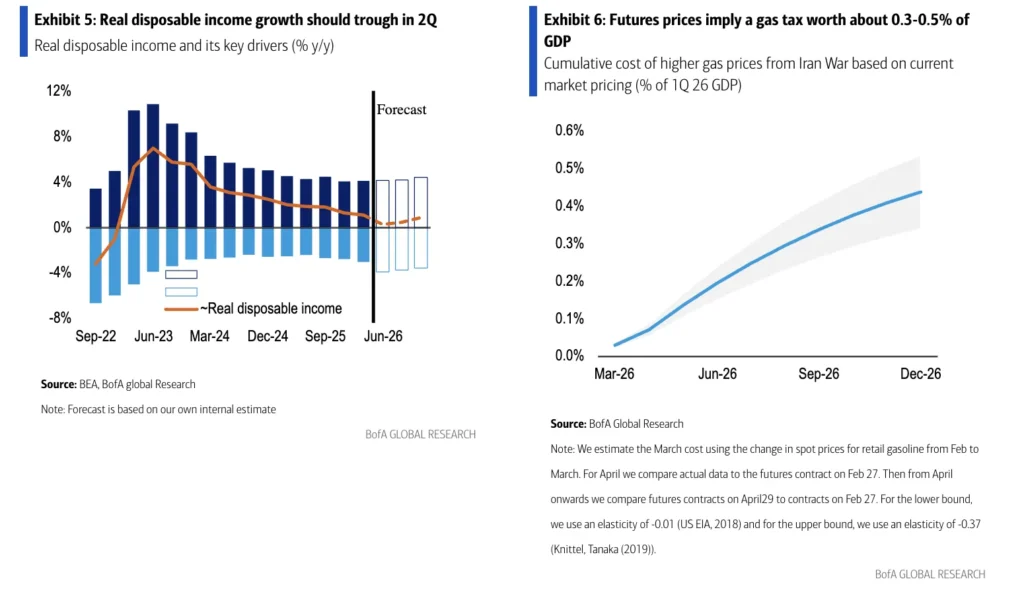

He estimates that oil prices would translate into a roughly 1% quarter-on-quarter, annualized decline in real after-tax income in the second quarter. At the same time, the savings rate is already low at 3.9%, so people have limited capacity to absorb this shock. Futures are pricing ever more expensive gasoline at the end of this year:

Source: Bloomberg

Confidence that the consumer and the broader economy can weather the energy shock rests on the assumption that oil prices don’t push up much further. Aditya Bhave of Bank of America notes that higher gas prices have already eroded nearly half of the income boost from tax refunds; to gauge the road ahead, he compares current wholesale gasoline futures with levels observed on Feb. 27, before the war, to estimate the additional burden on households:

We estimate the full-year “gas tax” to be around 0.5% of GDP. That is about equal to the boost we estimate from the One Big Beautiful Bill or AI capex. This drag could be much higher as we only focus on gasoline, and the energy shock should drive up the costs of other goods and services.

Futures may be unduly pessimistic. But if the shock is more persistent, then growth in disposable income could go negative, as the chart shows:

For now, the mega-caps’ capex is masking the disparity between the haves and have-nots. The troubles beneath this surface get bigger the longer the war drags on without any meaningful off-ramp. The weekend’s unraveling of Spirit Airlines — a low-cost airline for those on the wrong side of the K and reliant on cheap jet fuel — shows that the US is less exposed than others, but not immune.

—Richard Abbey

Share This:

More News Articles

{kind=link}

{kind=link}