Europe will need 65 more carbon dioxide (CO2) carriers and 33 new ports by 2050 to meet carbon capture, utilisation and storage (CCUS) goals, according to a new report from energy consultancy Xodus Group.

The report predicts that the overall European captured CO2 transport market will evolve from 2030 to 2050 as a hybrid system between a range of onshore and offshore transport methods.

The analysis screened roughly 850 operating ports across Europe down to a shortlist of around 200, identifying up to 60 that are well placed to gather captured emissions and route them to offshore storage by 2050.

The findings come as Europe seeks to scale carbon capture infrastructure from a handful of early projects to a continent-wide network.

Industry estimates suggest hundreds of CCUS projects are now in development globally, but transport and storage infrastructure is increasingly viewed as a key bottleneck to deployment.

Even if announced projects proceed as planned, global carbon capture capacity is expected to remain well below levels required under net-zero pathways by 2030.

And new CCS project announcements in Europe have in the last three years, according to research from the Institute for Energy Economics and Financial Analysis.

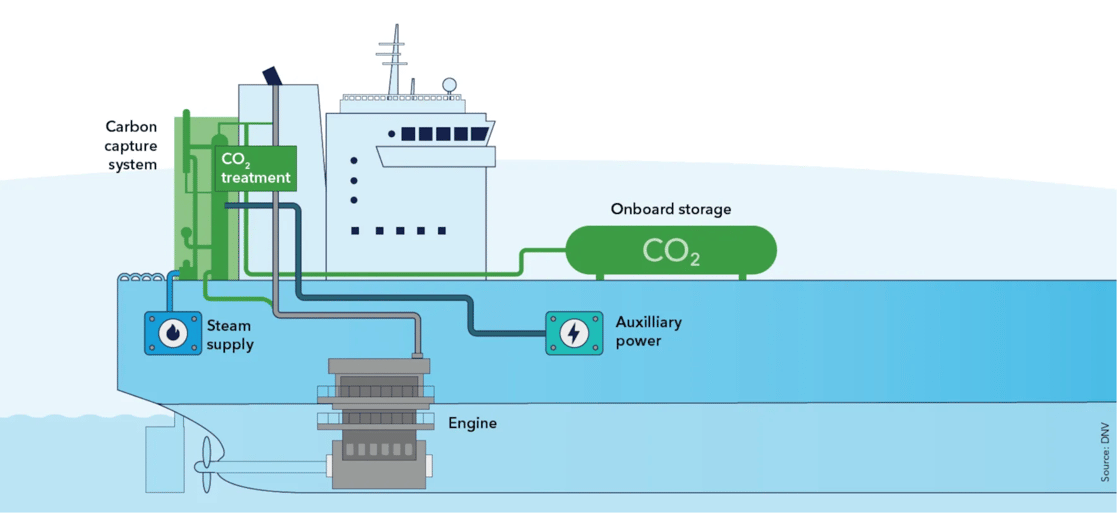

Non-pipeline transport such as shipping is key to building a cost-efficient European CCUS infrastructure network, according to the report.

The modelling suggests that, despite the market share for shipping decreasing over time from 48% to 24%, the estimated volume of CO2 transported by ship will increase over time, with up to 79 million tonnes per annum predicted by 2050. Pipelines are expected to dominate high-volume, heavily industrialised corridors.

The North Sea is expected to be the dominant CO2 sink across Europe, despite other maritime regions playing a major part in the overall market.

According to the North Sea Transition Authority, the North Sea basin could have a carbon storage capacity exceeding 150bn tonnes.

James McAreavey, Global Head of CCUS and Special Projects Lead at Xodus said that most of the technology needed to move captured carbon around Europe already exists and has been proved in the liquefied petroleum gas industry.

©Xodus Group

“The task now is scaling it,” he said. “Shipping gives emitters early access to offshore storage years before onshore pipeline networks can be consented and built.”

“If investment in ports and vessels starts now, the North Sea can set the benchmark for how the UK and Europe connected emitters to storage.”

And moves are being made for ship-based CO2 transport. In April, the Northern Lights carbon capture and storage joint venture liquefied CO2 carrier to its fleet.

“With our first two ships already in operation, [our third ship] Northern Phoenix marks the next step in scaling our CO2 shipping capacity,” said Tim Heijn, Managing Director of Northern Lights.

Two were signed in January where UK and European ports shared plans to study the potential of CCS shipping corridors between the UK and continental Europe.

The deal will see partners designing port infrastructure for CO2 handling, storage and shipping, in addition to building a value chain for transport between Associated British Ports Humber ports and European ports.

“This is not just about reducing emissions – it’s about creating a new market for carbon shipping that will help Europe meet its climate goals and secure industrial competitiveness … at pace,” said Henrik Pedersen, CEO of ABP.

Last year, Europe’s first offshore CO2 carrier, , received its final outfitting ahead of entering service on the Danish North Sea as part of Project Greensand – a cross-border CCS project led by INEOS Energy and Wintershall Dea.

{kind=link}

{kind=link}