Uranium enrichment explained

Urenco was established in 1970, and is one-third owned by the UK government, one-third by the Netherlands and one-third by the two German utilities RWE and Eon. It provides uranium enrichment services, which is the third stage of the nuclear fuel cycle (after mining of uranium and conversion, but before the fabrication phase).

Unenriched, or natural, uranium contains about 0.7% of the fissile uranium-235 (U-235) isotope. (“Fissile” means it’s capable of undergoing the fission process by which energy is produced in a nuclear reactor). The rest is the non-fissile uranium-238 isotope. Most nuclear reactors need fuel containing between 3.5% and 5% U-235. This is also known as low-enriched uranium, or LEU. Advanced reactor designs that are now being developed – and many small modular reactors – will require higher enrichments still. Material containing between 5-10% U-235 is known as LEU+ and high-assay low-enriched uranium, or HALEU, covers enrichment up to 20%.

Enrichment increases the concentration of the fissile isotope by passing the gaseous uranium hexafluoride through gas centrifuges, in which a fast spinning rotor inside a vacuum casing makes use of the very slight difference in mass between the fissile and non-fissile isotopes to separate them. As the rotor spins, the concentration of molecules containing heavier, non-fissile, isotopes near the outer wall of the cylinder increases, with a corresponding increase in the concentration of molecules containing the lighter U-235 isotope towards the centre. contains more details about the enrichment process and technology.

Urenco’s expansion plans

Earlier this month Urenco USA announced that its facility in New Mexico, which is currently the only commercial uranium enrichment capacity in the USA, is to see its capacity increased by 2.1 million SWU (Separative Work Unit – the standard measure of the effort required to separate U235 and U238 – see and World Nuclear Association’s for more information about uranium enrichment).

Together with expansion plans in the Netherlands and Germany that means Urenco is adding 4.6 million new SWU, all built on the strong order book, “stable policies and the support and confidence of our customers”. The extra capacity will come online over the next six years or so.

Things have definitely changed quite dramatically since 2020, notes Odeh.

“We were planning to be a smaller company in 2030 than we were in 2020, for the reason that there was ample over-capacity in the enrichment market. Prices were depressed and therefore we were just planning for as soft a landing as we could in terms of capacity. Then several factors came into play that have completely changed the landscape for nuclear and therefore for enrichment. The first one was decarbonisation. There was a clear drive to decarbonise, and the pledges signed at COP28 (to at least triple global nuclear capacity by 2050) clearly showed political willingness to enter into nuclear again. The war in Ukraine has put the spotlight on energy security and energy independence as well, and people have realised that nuclear can be, and should be, part of the mix to ensure energy security. And finally, you can see reliance on fossil fuel at the moment, with the extreme volatility that we see in the oil and gas market, is also an element that played in favour of nuclear.

“So this whole chain of events has changed completely the landscape, the view towards nuclear. So now people, countries, utilities are looking at nuclear again. And that was post the start of the war in Ukraine.

“You can also see another factor, which is the extreme growth of electricity demand, especially in the United States, based on data centres for AI being built, that need baseload power, 24/7 decarbonised electricity. And that’s where nuclear has a role to play. And therefore, if nuclear has a role to play, we as an enricher of uranium, we too have a role to play.”

(Image: Urenco)

Odeh says there is a strong link between the order book and expansion plans: “We’re relatively lucky in the nuclear business. When people build a large nuclear power plant, you can see the demand coming. So you can adapt and adjust your capacity accordingly to serve that market. We take a punt as well, but of course, the stronger the order book, the more confidence we have in our capacity expansion.”

And the long lead time for nuclear new-build helps too. “It’s quicker to expand an enrichment facility – basically we replicate modules that look exactly like the previous one – than it is to build a nuclear power plant,” he says.

Having said that, there is the prospect of small modular and advanced modular reactors which should be quicker to build. Odeh says Urenco is ready to adapt its business model if necessary if much quicker build-times emerge for 4th generation reactors.

Urenco uses centrifuges to enrich uranium, but what about innovative new tech being trialled or piloted, like laser enrichment or chemical enrichment processes?

Odeh says: “We are quite well placed to know that there could be disruptive technologies that change the market entirely. In 2000, it was gas diffusion plant that was the main technology to enrich uranium, and then the centrifuges became more efficient, more effective, and therefore suddenly the centrifuge became the workhorse of the industry and still is today. We continue to believe that the centrifuge technology will remain the workhorse.

“Having said that, we always monitor what the competition is doing. We always monitor the potential new technologies. We’ve made a small investment in Ubaryon, as you know, a chemical enrichment potential. But at the moment there is no intention for Urenco to change the main technology we use, which is the gas diffusion centrifuge.”

How significant does he see the recently announced capability to produce LEU+ – material containing between 5% and 10% U-235 – in the UK and the USA?

“It’s a significant step because you can see today, and we talked about it earlier on, it takes a long time to add capacity to build a new reactor, a traditional reactor, a large-scale reactor. Therefore, utility customers, if they want to increase their output, they are looking at what can we do. And one way to do that is to produce fuel using LEU+, a higher level of enrichment, to increase the burnup, to increase the length of the cycle, and to reduce the number of outages. So quite a few utilities in the world, and particularly in the US, are looking at this new kind of product. So come next year, we’ll have two facilities out of the four we operate today that are capable of producing LEU+.”

There is also the future need for HALEU fuel and Urenco’s project at Capenhurst to have the first European commercial-scale facility. How is it progressing?

“It’s progressing fairly well. We have launched the first HALEU commercial-scale facility at our Capenhurst site, together with the UK government that co-funds this facility. For HALEU, it’s a bit more of a challenge because the market is nascent. You don’t have a mature market. So you’ve got quite a lot of reactor developers that need HALEU fuel but they are not yet established. They don’t always have the construction licence. So it’s quite difficult for a private company like us to invest hundreds of millions of euro/pounds/dollars into a facility when you don’t know exactly where and to who you’re going to sell it to. The UK government helped us to basically solve this chicken and egg problem. So we’re building. We’re on track to have the output and the facility online in 2031. We are discussing with a few reactor developers for their trial of fuel. And should that market take off, we have the opportunity to expand, again, using the same modular approach that we’ve done in the past to be able to build whatever the market needs.”

With large-scale reactors there are about five or six main designs in the market, compared with 80 or so for SMRs and AMRs. Odeh says: “So there will need to be some level of consolidation, rationalisation, because everyone’s got a different type of fuel, different type of cycles.”

Does Urenco ever consider entering other parts of the fuel cycle?

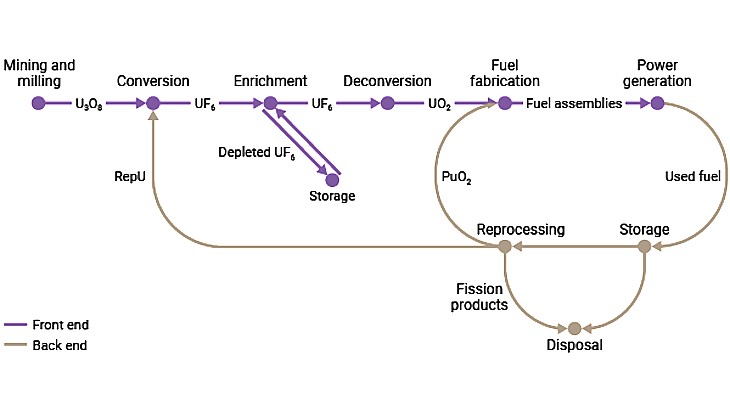

A graphic showing the main nuclear fuel cycle stages (Image: World Nuclear Association)

“There’s always a question of vertical integration … competitors sometimes are vertically integrated. The one thing we know is enrichment. We know how to do it and we do that fairly well. We’ve had, from time to time, discussion about what’s the strategic positioning of the company. The focus remains on enrichment, providing enrichment services. There aren’t that many companies in the world that can provide those services. So we see that as our duty, as well as to be able to expand and deliver the critical services that utilities need. And of course, we are good nuclear stewards as well. So when you do enrichment, you end up with two streams of product. One is enriched uranium product, the other one is depleted UF6. So we’ve also built a tails management facility on our site in Capenhurst that we are looking to expand, because the more enrichment demand you have, the more depleted uranium you produce. We are doing deconversion of UF6 into oxide, a more stable form for long-term storage. That can be re-enriched in the future, if market circumstances change. But those are the two main things that we’re working on.”

The medical isotopes business is also a priority for Urenco. “It’s a smaller, much smaller, business, but very critical when it comes to research, medical applications – every year millions of people use our product for either diagnosis or treatment, so it is something that we’re very proud of,” says Odeh.

And does he think that there will be sufficient nuclear fuel were there to be a tripling of nuclear capacity by 2050?

“Yes, simply put, yes. As I said, it takes a lot less time to build an enrichment hall than it is to build a nuclear reactor today. We’ve got our sites licensed for more capacity than they currently operate under, and therefore we’ve got the potential to expand our sites and our facilities. We’ve already announced equivalent to 4.6 million SWU of additional capacity. It’s a significant undertaking. If we’re talking about tripling nuclear by 2050, and the US is even talking about quadrupling their own nuclear capacity – let me put it this way, that’d be a nice problem to have for us.”

Will there be enough uranium to enrich though?

Odeh says: “You need to start exploration today to find the new deposits, but what we’ve seen recently is more budget being allocated to exploration. It takes a long time to build a nuclear power plant. It takes a long time to bring a new mine online too. So those things need to happen in parallel. But there is a lot of uranium in the world. You just need to find the right deposit and to be able to mine it economically. So I think the fuel cycle is working. The nuclear industry forces you to think about not the next three years, the next five years, but the next 20, 30, 40 years. So I’m very hopeful that our colleagues in uranium mining are doing the right thing in terms of allocating significant budget for exploration. We will, when it comes to enrichment, be able to expand accordingly. As I said, I have no doubt that we can step up.”

What would be his ask to governments to help facilitate nuclear capacity expansion?

“What I’m asking government to consider is to have a level playing field. Competition is good, but it has to be a fair competition. For years, there has been no reciprocity between ourselves in the Western world and non-OECD countries when it comes to enrichment product and prices. And we’ve seen a lot of product being dumped into the market at depressed prices. Now the US has taken a bold decision in putting a Russian ban in place from 1 January 2028. That gave us the visibility and enabled us to trigger investment, because you know that you’re going to invest hundreds of millions, billions of dollars, but that suddenly you won’t have a wave of product coming onto that market. So the US has done that. Now we’re looking at Europe, which is the other key market we operate in. We work everywhere, but our two key markets are the US and Europe. And in Europe, there is this discussion about Repower EU (the potential EU energy-related legislation]. We’re yet to find some clarity on that front. So people are asking us to invest, to add on capacity, but we also need the right ingredients in terms of policy to make sure that, should we invest and trigger significant investment, we won’t find ourselves five years down the road with waves of volumes coming from non-OECD countries at depressed prices, which will then depress the entire market and force us to book impairment as we did in 2016 and 2017 on our US asset.”

There is a widespread goal of at least tripling of global nuclear capacity by 2050. Will the target be achieved?

“I think there will be more installed capacity in 2050 than there is today. Tripling is a very significant ask. Again, it takes some vision. Nuclear is not a policy you decide and then you flip-flop at every election cycle. You need to have a clear view. I was born and raised in France. After the oil shock in the 1970s, there was a clear, serious nuclear plan, building the series effect, boom, boom, boom. And then you’ve got the learning, you gain experience alongside, you’ve got a strong supply chain that can be mobilised. You look at what’s happening in China at the moment, that’s exactly what’s happening. You’ve got six or seven reactors being switched on every year, rigorously. It’s the same for other countries. It’s a significant undertaking, but energy demand is coming up, electricity is going up. If you want carbon-free, reliable base-load power, nuclear has to be part of the solution. So whether it’s tripling or not, I will not comment just yet. I think it’s a very, very strong ambition, but I’m convinced that there will be more installed capacity. And even doubling nuclear when compared to today will be a significant achievement. If more can be done, great.”

You can listen and subscribe on all major podcast platforms:

Episode credit: Presenter Alex Hunt. Co-produced and mixed by Pixelkisser Production

Email newsletter:

{kind=link}

{kind=link}