The Independent Commodity and Intelligence Service (ICIS) has delayed its forecasts on the return of Qatar and UAE liquefied natural gas to market to October.

Before the , it had forecasted Qatari output returning in August, ahead of maximum output in September.

The readjustments in expected LNG supplies for August and September will have major implications for the global economy and energy sector.

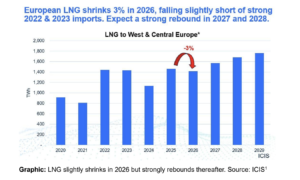

Around 5 to 6 million tonnes of LNG output will be lost for every extra month that Qatar and the UAE are offline, according to ICIS. With the downward revision of Qatari LNG supply, it estimates European LNG imports to shrink slightly by -3.2% year-on-year, but anticipates a strong rebound in 2027 and 2028.

©ICIS

“Alternative new sources of supply have also been slow to build up this year,” it notes.

“The biggest expected new supply this year was Qatar’s own expansion, which is now delayed into H2 2027 or beyond. The next biggest addition was the US Golden Pass plant, which had been hoped to bring on one or two 6 mtpa trains this year and later a third, to reach 18 mtpa capacity. So far this year Golden Pass has only loaded four cargoes, one each month , May, June and July, compared with around seven per month if the first 6 mtpa train was operating full.”

With Europe’s gas storage remaining low, the global LNG tightness fuels a sense of urgency for storage refilling and poses concerns for the winter ahead – but ICIS projections indicate European gas storage can still reach November targets even under a .

Though it comes at a price. ICIS modelling suggests TTF would need to average around €54/MWh during the storage-filling season to attract sufficient LNG to Europe and sustain storage injections.

“Under both our base case and cold winter scenarios, European gas storage reaches around 80% fullness by 1 December 2026. While this remains consistent with the lower end of the EU storage regulation and provides a solid proxy for security of supply, the market must increasingly pay for this outcome through higher gas prices,” it adds.

ICIS’ total 2026 LNG supply forecast is now around 431 million tonnes, down from 441 million tonnes previously.

Separate analysis from S&P Global forecasts over the next five years, making LNG the country’s second-largest net export industry.

The helium industry is also dependent on the resumption of Ras Laffan operations, with Qatar accounting for around a third of global helium supply.

China plans for helium based on changes in domestic and international supply and demand, according to a Ministry of Commerce spokesperson.

{kind=link}

{kind=link}