By

56 min ago 3 min read

US liquefied natural gas (LNG) export capacity is projected to double over the next five years, making LNG the country’s second-largest net export industry, according to a new study published by intelligence firm S&P Global Energy.

The US is currently the leading supplier of LNG globally, with exports totalling $44bn in 2025. By 2031, it is expected to capture over a third of the global market share.

S&P Energy believes that US feedgas demand for LNG shipments will double to 36 billion cubic feet per day (bcf/d) in the next five years, 25% higher than previous base case projections.

Domestically, seven new projects are targeting a final investment decision, with several new developments expected within the next six to twelve months.

If this growth continues, S&P Global projects total investment in the US LNG supply chain will reach over $1 trillion and contribute $1.4 trillion to gross domestic product through to 2040.

Additionally, it expects future LNG export activity to generate more than $2.9 trillion in total revenues for US businesses, in addition to $206bn in federal and state tax revenues.

Over the next five years, $19bn of LNG-related investment is expected to be deployed.

US LNG pause

In January 2024, then US President Joe Biden announced a on approving new LNG export projects under an executive order.

The pause, lifted in January 2025, allowed the US Department of Energy (DOE) to review its authorisation protocol.

S&P Global said under an “extended pause” scenario, where the $44bn in US LNG exports were not executed in 2025, the global LNG market would tighten, pushing prices 50% higher for European and Asian LNG importers by 2031.

If the extended pause had been put in place, S&P Global believes the US would have effectively transferred $76bn per year to non-US LNG suppliers, who would have filled the market deficit with mostly fossil fuels.

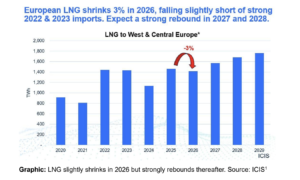

According to a from the Institute for Energy Economics and Financial Analysis (IEEFA), under current conditions, the US could supply 80% of European LNG imports by 2028.

US and Russia LNG market share

S&P Energy expects that the extended pause scenario in US LNG exports would likely benefit Russia.

In the case of an extended pause, US LNG would decrease by up to 10 bcf/d, and up to 14 bcf/d of underutilised Russian pipeline and LNG export facilities would be positioned to potentially fill the market deficit.

S&P Energy said that without US LNG exports, securing the EU ban on Russian LNG and gas would have been difficult, considering the underutilised Russian capacity and loss of confidence in the US market.

In December 2025, the European Council and Parliament reached a provisional agreement to imports of Russian LNG and natural gas, with a full ban from the end of 2026 and autumn 2027, respectively.

US LNG exports replaced half of Europe’s pre-war gas imports from Russia.

IEEFA’s European LNG Tracker shows Europe’s move away from Russian gas has tripled its reliance on US LNG between 2021 and 2025.

However, Russia remains the second-largest LNG supplier in the EU market, with Europe’s imports of Russian LNG reaching record levels in Q1 of this year, up 16% year-on-year, driven by deliveries to France, Spain, and Belgium, IEEFA data shows.

{kind=link}

{kind=link}